Homeowners and Condominium associations eventually face the same reality as any building owner: major items wear out. Roads deteriorate, roofs reach the end of their useful life, pools need renovation, and mechanical systems fail. These projects can cost tens or even hundreds of thousands of dollars.

If a community does not plan ahead, paying for repairs and replacements could mean a huge, surprise special assessment for homeowners. But when associations plan responsibly using reserve funding and reserve studies, the cost of maintaining the community can be distributed fairly across owners over time.

Understanding how reserves work helps homeowners see why they are one of the most important financial tools in community association governance. If you are dealing with an abusive Board, chances are they are also cutting corners with your community’s reserve fund–if they have one at all. It is common for Boards to ignore adequately funding reserves in order to keep dues low. The reserves should be one area concerned homeowners should keep tabs on. The costs of not doing so can be brutal.

Reserves are funds set aside by the association specifically to pay for major repairs and replacements of community owned property. They should be held in a separate account from the association’s regular operating account. The operating budget typically covers routine annual expenses such as mowing, snow removal, insurance, taxes, utilities, and minor repairs.

Reserve funds, by contrast, are intended for large capital expenses that occur periodically but not every year. Common reserve-funded projects include roof replacement, road or parking lot resurfacing, exterior painting or siding replacement, elevator upgrades, pool renovation, HVAC or boiler replacement, or fence replacement.

These components have predictable life cycles. Even if the exact timing varies slightly, it is certain they will eventually require replacement.

A reserve study is a long-term planning document that describes what major components must be maintained, when those components will likely need replacement, how much those replacements will cost, and calculates how much money should be saved each year.

Reserve studies are typically prepared by engineers, reserve specialists, or other professionals experienced in construction systems and financial forecasting. Most reserve studies contain two parts: a physical analysis and a financial analysis..

1. Physical Analysis

The physical analysis identifies and evaluates the major common components the association is responsible for maintaining. For each component, the study usually estimates the current condition, total expected useful life, the remaining useful life, and the estimated replacement cost.

This information helps create a long-term maintenance and funding roadmap for the community.

2. Financial Analysis

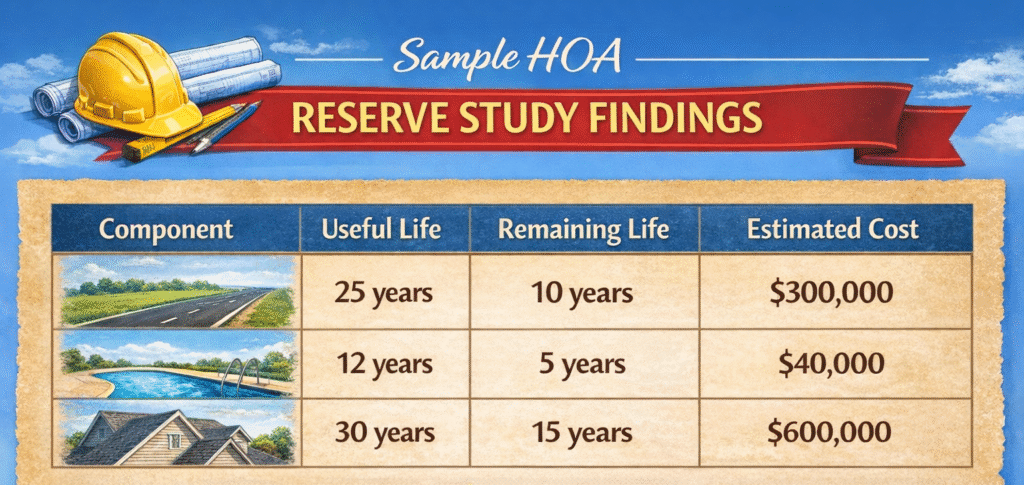

The financial analysis section of the reserve study converts the physical findings into a funding plan. It calculates how much the association should contribute to reserves each year so funds will be available when major components need replacement. For example, if a roof replacement is expected to cost $600,000 in 15 years, the association should ideally save about $40,000 per year toward that project. The reserve study aggregates similar calculations across all components and recommends a total annual reserve contribution for the association.

Reserve funding is widely considered the fairest system for allocating long-term maintenance costs among homeowners. The reason is simple: it spreads costs across the people who actually benefit from the property during its lifespan.

What Happens Without Reserves

Imagine a community road that lasts 25 years and costs $300,000 to replace. If the association does not save for the project, the owners living in the community in year 25 could suddenly face a $300,000 special assessment. Those owners might have lived there only a few years, yet they would bear the entire cost of wear and tear that occurred over decades.

What Happens With Reserves

With proper reserve funding, the association saves money each year during the road’s life. Each homeowner contributes a small portion of the replacement cost through regular assessments while they live in the community. This means costs are shared across generations of owners. No single group of residents bears the entire burden. Financial planning becomes predictable and manageable

In effect, reserve funding works like saving for depreciation of community infrastructure.

Reserves do more than prevent special assessments.They also support financial stability and property values. Communities with properly funded reserves tend to experience fewer financial surprises, better-maintained buildings and infrastructure, greater buyer confidence, and stronger mortgage eligibility for purchasers.

Mortgage lenders and insurers often review association finances during real estate transactions. Underfunded reserves can signal future financial problems, which may affect lending decisions.For this reason, many buyers and real estate professionals consider the reserve balance and reserve study when evaluating a community.

When reserves are ignored or underfunded, it becomes more likely that the community will fall behind on maintenance and replacement tasks. This issue led to the collapse at the Champlain Towers South condo in Surfside, Florida in 2021.

In addition to common element failure, failing to keep up with reserve funding may lead to the Board issuing special assessments of thousands of dollars to each homeowner to cover critical repair projects. Many homeowners are on fixed incomes and cannot cover that unexpected bill.

Legal requirements vary significantly depending on the jurisdiction. Maryland and DC take very different approaches.

Maryland Law on HOA Reserves and Reserve Studies

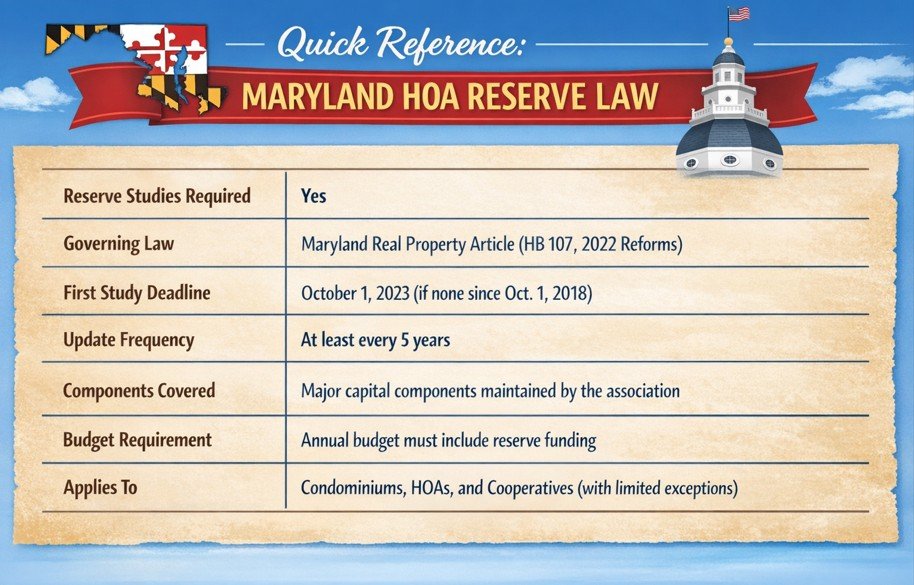

Maryland now requires most community associations to conduct reserve studies and fund reserves. In 2022, Maryland passed updated legislation which expanded reserve study requirements for condominiums, homeowners associations, and housing cooperatives.

Under Maryland law associations must conduct a professional reserve study identifying major capital components. The initial study generally had to be completed by October 1, 2023 if the association had not conducted one since October 1, 2018. Reserve studies must be updated at least every five years thereafter. The study must identify major components the association must maintain, remaining useful life of those components, estimated replacement costs, and the recommended annual reserve contributions.

Maryland law also requires associations to include reserve funding in their annual budgets consistent with the reserve study recommendations. This means that, in Maryland, associations cannot simply ignore long-term infrastructure costs. The law requires boards to identify future obligations and create a plan to fund them.

Pursuant to a change in the law in 2025, Boards may, after a ⅔ majority vote, determine that the association is experiencing a financial hardship that is limiting the ability to fund the reserve and may temporarily adjust the amount deposited.

Some limited exceptions to the reserve funding and study mandate exist—for example, small communities with minimal common property—but most associations maintaining shared infrastructure must comply.

District of Columbia Law on HOA Reserves

DC takes a less strict approach to reserve funding and reserves studies. The DC Condominium Act permits associations to maintain reserves but does not require reserve studies or mandate a minimum reserve funding level.

Instead, DC law focuses primarily on budgeting and financial disclosure. Associations must provide financial information to owners and prospective purchasers, including reserve balances, but the statute does not require a reserve study, a minimum funding percentage, or a specific update schedule. As a result, reserve planning in DC is largely driven by best practices, lender expectations, and the association’s governing documents.

Many professionally managed DC communities still conduct reserve studies every three to five years because it helps boards plan major repairs and avoid special assessments.

Across the country, lawmakers have increasingly emphasized reserve planning for community associations.

One reason is concern about aging buildings and deferred maintenance, particularly in older condominium communities. Reserve studies provide transparency about future costs and encourage associations to address those costs gradually rather than waiting for a crisis.

Maryland’s reserve study law reflects this growing policy trend: communities are expected to plan for the long-term maintenance of shared infrastructure.

Reserves and reserve studies provide a structured way for homeowners’ associations to plan for inevitable major repairs. By identifying future expenses and saving gradually over time, associations can avoid sudden financial shocks and maintain community infrastructure responsibly.

Perhaps most importantly, reserve funding promotes fairness among homeowners. Each owner contributes toward the long-term maintenance of the community during the time they live there, rather than shifting the entire burden onto future residents.

For communities that want stable finances, well-maintained property, and predictable assessments, reserve planning is not just good practice—it is an essential part of responsible HOA management.